The Housing Rehabilitation Loan program is available to low and moderate-income homeowners for taking care of health, safety, and maintenance issues with their existing homes.

This program comes from both federal grants and local revolving loan funds to provide suitable living environments and expand economic opportunities for low and moderate-income households.

Repairs may include, but are not limited to:

Plumbing

Electrical

Structural repair

Roof Repair/Replacement

Siding

Paint

Windows/Doors

Insulation

HVAC

Frequently Asked Questions

How do I pay for these repairs?

This a loan program and qualified applicants will have a lien recorded against their homes in the amount of construction and loan fees. The loan is interest-free and requires no repayment as long as the borrower is living in the home. Repayment is required when the borrower moves out of the home, sells the home, or is deceased. Repayment is only accepted as a lump-sum payment. Early repayment is accepted.

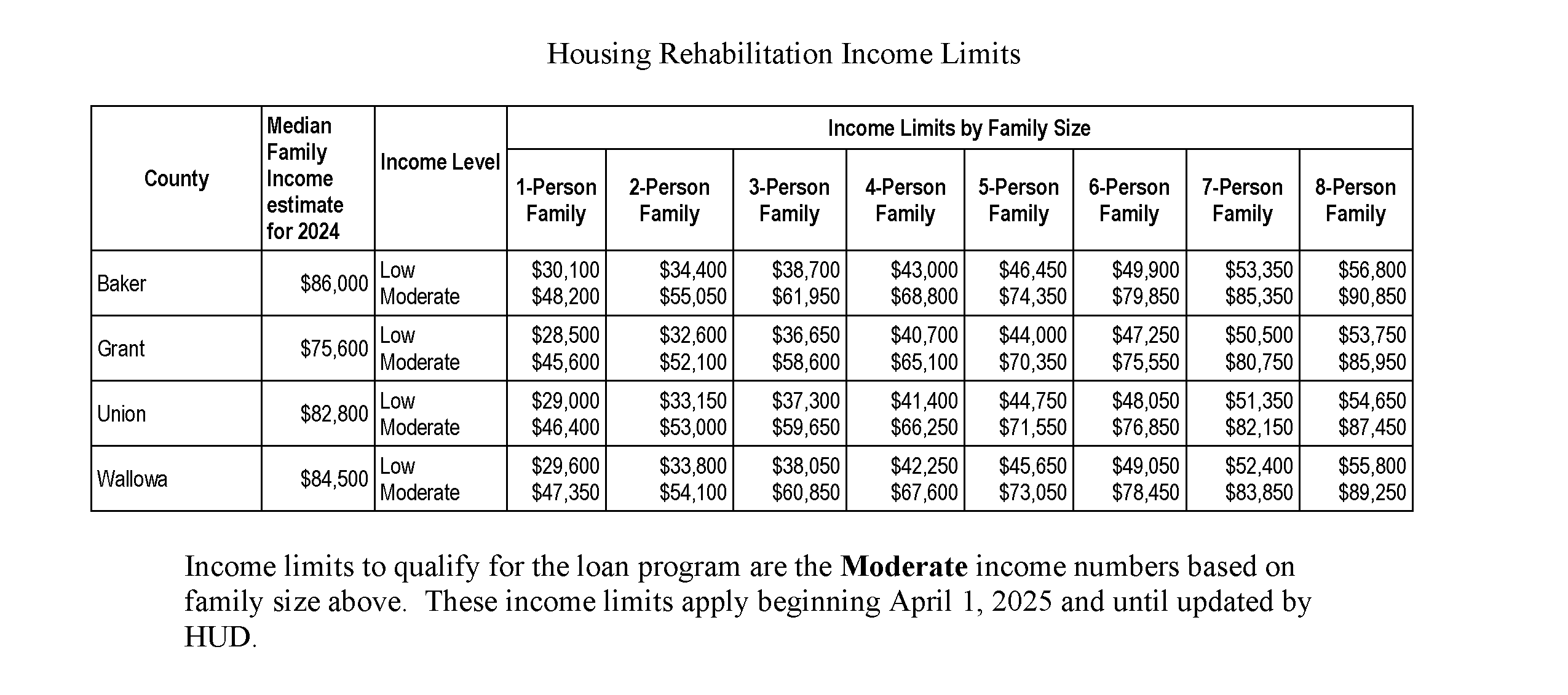

What are the eligibility guidelines?

Must own or be buying your home

Real market value of home must not exceed $250,000

Manufactured homes built after 1976 will be considered if they are on the resident’s property and de-titled

Owner must have sufficient equity

Your home value must be greater than outstanding home loan by enough to fund the project and leave some equity in the home

Homes in a flood hazard area must have and maintain flood insurance for the life of the loan

Brief overview of the rehabilitation process

Pre-Application

Processed by Community Connection, including:

Initial screening of applicant income

Initial screening of home value and equity status

Full Application

Processed by Community Connection, including:

Property title search for other encumbrances, such as tax liens or judgements

Flood hazard determination

Credit report

Proof of income

Proof of insurance

Home Audit

Home inspection by the Community Connection auditor/inspector, including:

Thorough inspection of home

Interview with homeowner

Create a list of necessary and eligible repairs and improvements

Photographs of home

State historic preservation office review

Project review by local building department

Contractor Bidding

Homeowner send completed bid sheets to local contractors for bidding

Contractors submit big to either homeowner or Community Connection

Homeowner chooses successful bidding contractor

Construction Contracts and Loan Documents

Construction contract and accompanying documents signed

Loan documents signed, notarized, and recorded

Construction

Contractor will have 90 days to complete contracted work

In-progress and final inspections performed by Community Connection’s auditor

Inspections on permitted activities by local building official or inspector

Where can you call or apply for housing rehabilitation?

{kind=link}

{kind=link}

{kind=link}